Question: when does a loan become a contribution?

Campaign finance laws are numerous and not always black and white. How many candidates do the very same thing that Matt Kealty has done and not even know it? As I understand it, Matt borrowed money to finance his campaign for Mayor. He signed documents stating when payments are due and interest to be paid. This was no different than a Mortgage loan, Bank Credit Card, Car Loan, Student Loan or for that matter any other type of debt instrument.

Let us take a look at a theoretical candidate. They wish to run for office and have stocks that are doing well, but they do not wish to sell any. They decide to borrow money against the equity in their account. They can open a margin account and draw on this to buy more stock or take out cash. If they take cash out and contribute it to their campaign, must they report this new “loan” owed to a brokerage firm as being obtained from the brokerage firm?

What if the person has a home equity loan? They can use this borrowed money for any purpose, no questions asked. They could contribute it their campaign. Again, what is the correct method of reporting? The candidate is on the hook for the money they borrowed, but are they required to identify the source as being XZY mortgage company/bank?

What if the candidate is out on the town with just $100 in their pocket? They take the family out to dinner and instead of paying cash, they charge it and they contribute the $100 to their campaign. Are they required to identify the source as being the credit card company?

My question is pretty basic, how far back do you trace the origin of contributions? Is the basic premise of the campaign law to identify who is contributing money to which candidate and if so, is a loan the same thing as a contribution?

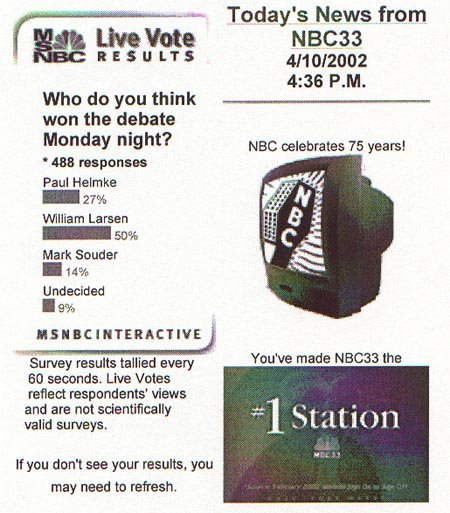

posted by William Larsen @ 11:47 PM

![]()

![]()

0 Comments:

Post a Comment

<< Home